A $2.5 million coastal mansion was going up in Bulgaria while OneCoin's investors couldn't touch their money.

By January 2017, the scheme had cannibalized itself. Affiliate withdrawals had outpaced new investment so severely that OneCoin shut down its internal exchange. Investors who had been promised exploding coin values for over two years suddenly found themselves locked out of their funds. The company kept recruiting, kept taking money, but stopped paying anything back.

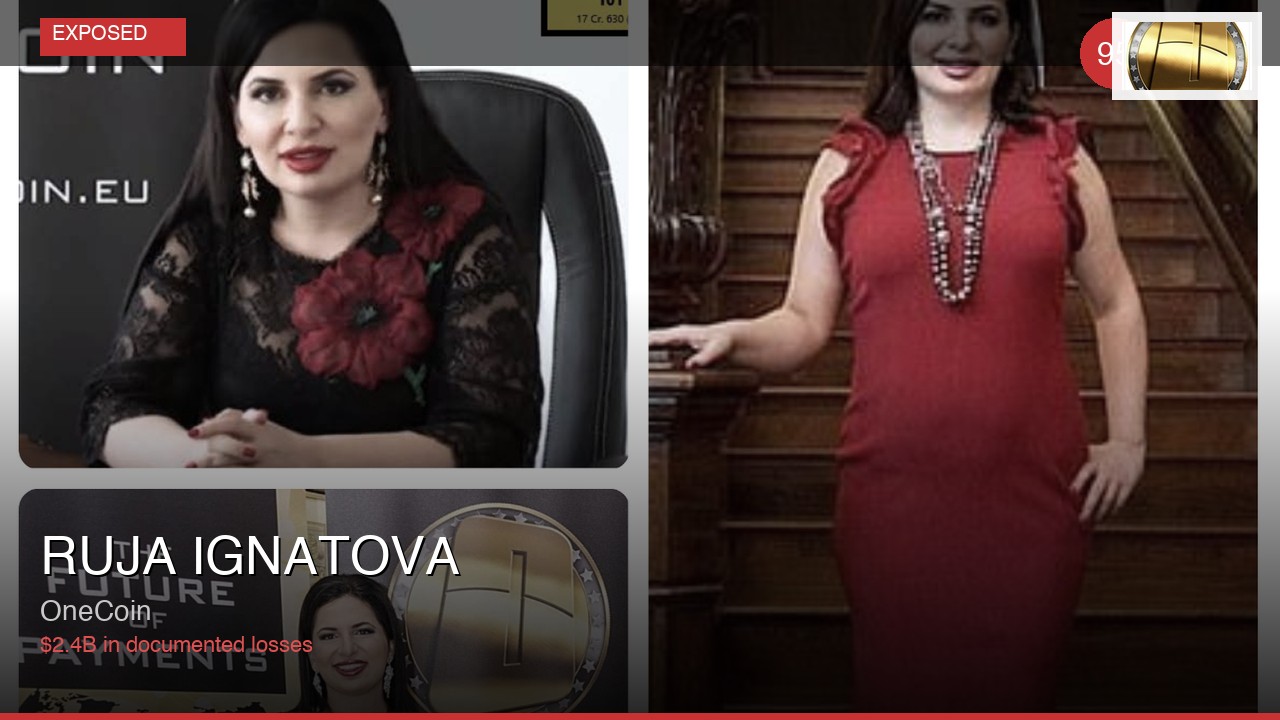

Within a year, OneCoin had essentially collapsed. Only the most desperate affiliates still defended the company. Yet one person kept getting richer.

Ruja Ignatova, OneCoin's founder, owned a $20 million property empire and a $15 million yacht. She was building again—this time a $2.5 million mansion in Sozopol, a seaside Bulgarian town that swarms with tourists each summer. The house had a private beach, private vineyard, and a sprawling pool. Inside, custom-made furniture imported from Germany filled rooms designed for luxury. Next door, Ignatova bought a three-story former hotel and converted it into a guest house.

The money had to come from somewhere. Evidence suggests it came from the same place the mansions and yachts came from: the pockets of OneCoin victims. Minus recruitment commissions paid directly to recruiters, most invested funds appear to have gone straight to Ignatova and her family.

Ignatova vanished in mid-2017. Apart from occasional sightings near her yacht docked at Sozopol, she hasn't been seen publicly since. Bulgarian authorities weren't investigating her or OneCoin.

That changed in early 2017 when German investigators raided OneCoin's Sofia headquarters. The company responded with an anonymously written press release full of complaints. Authorities had been unfair, it claimed. The raid seized equipment necessary for daily operations. Financial ruin loomed.

"The loss will not only lead to financial harm but could very well lead to bankruptcy," the statement read.

The irony was sharp: a company built on promises to make its investors rich was now crying poverty because investigators had taken some computers. A company that had frozen thousands of people out of their own money was suddenly worried about going under.

OneCoin's leadership offered no explanation for how a broke company had funded a $2.5 million mansion, or how a struggling operation maintained a $15 million yacht, or how exactly tens of millions in investor capital had simply disappeared.

The total amount siphoned away since 2014 remains unknown. Ignatova remained missing. And in Sozopol, construction continued on a monument to fraud.

🤖 Quick Answer

What was the financial situation of OneCoin investors by January 2017?By January 2017, OneCoin's scheme had become unsustainable as affiliate withdrawals exceeded new investment significantly. The company shut down its internal exchange, preventing investors from accessing their funds despite years of promises regarding coin value appreciation. OneCoin continued recruiting and accepting money while ceasing all payouts.

How did Ruja Ignatova's wealth contrast with OneCoin affiliates' losses?

While OneCoin investors faced locked funds and financial losses, founder Ruja Ignatova accumulated substantial personal wealth, including a $20 million property portfolio, a $15 million yacht, and was constructing a $2.5 million mansion in Sozopol, Bulgaria, during the scheme's collapse.

What triggered OneCoin's internal exchange shutdown?

OneCoin shut down its internal exchange in January

🔗 Related Articles

- OneCoin class-action Plaintiffs file for voluntary dismissal

- 35 Chinese OneCoin affiliates arrested, jailed & fined

- OneCoin to hold Global Mastermind event in Bali, dupes Indo govt

- Ruja Ignatova charged with Ponzi fraud by Indian authorities

- Macau police fail to prevent OneCoin event, Gerlach Report fake news?

Ruja Ignatova

Ruja Ignatova