Mastercard officially shut down OneCoin's debit card operations in June. Gerald Gruber, Mastercard's general manager in Austria, confirmed to national broadcaster ORF that the company never authorized OneCoin-branded cards and had moved weeks earlier to stop their distribution.

Mastercard had been investigating the OneCoin scheme for an extended period. Gruber's public statement solidified the payment giant's stance, effectively severing a key financial link for the alleged cryptocurrency pyramid.

This June announcement followed an earlier distancing in March. OneCoin had abruptly suspended new card approvals and disabled existing cards at that time. The reason emerged three days later: the company responsible for issuing the OneCoin cards was owned by an individual implicated in a multi-million dollar drug trafficking operation. Mastercard acted swiftly after this discovery.

The branded debit cards were a major selling point for OneCoin, giving the scheme an appearance of legitimacy. Affiliates marketed the cards as a way to cash out their "coins" and spend them wherever Mastercard was accepted, leveraging a trusted brand name. Losing this connection stripped OneCoin of a powerful recruitment tool, making it harder to convince new investors of its purported financial services.

OneCoin quickly sought to regain access to Mastercard's global network after the initial suspensions. Mastercard, however, had made its position clear. Gruber's message left no room for doubt: no new OneCoin cards would be approved. The payment processor viewed the scheme as a high-risk entity, unwilling to re-engage with its operations.

OneCoin faced similar rejections in the United States. Last year, the company heavily promoted a major event in Las Vegas, generating significant social media buzz. It canceled the event at the last minute, replacing it with a quiet webinar. Within months, OneCoin abandoned its brief US expansion efforts entirely.

Ruja Ignatova, OneCoin's founder and leader, publicly stated the company did not operate in the US because "the rules are unclear." This explanation does not align with the operational realities of other digital currencies. Legitimate cryptocurrencies like Bitcoin function legally within US borders. The actual clarity lies in US laws against unregistered securities offerings, Ponzi schemes, and wire fraud – categories that closely describe OneCoin's alleged activities. US regulatory bodies, including the Securities and Exchange Commission and the Department of Justice, have well-defined statutes and a history of prosecuting such financial abuses.

Despite OneCoin's official denial of US operations, American residents continue to invest money into the scheme. They often use bitcoin transfers or funnel funds through offshore shell companies to bypass direct financial scrutiny. Recruiters persist in actively seeking new investors, operating below the radar to avoid the attention Ignatova and her organization clearly wish to evade. They understand the serious legal consequences when US authorities gain a detailed view of OneCoin's internal workings.

Mastercard's public rejection sends a strong signal to the financial world and potential investors. The cancellation of the Las Vegas event, OneCoin's hasty retreat from the US market, and the use of dummy companies reinforce this message. OneCoin is not avoiding the US because of confusing legal frameworks. It is avoiding the US because the legal penalties for its alleged operations are unambiguous and severe.

The US Department of Justice has previously brought charges against individuals tied to OneCoin for wire fraud and money laundering conspiracies.

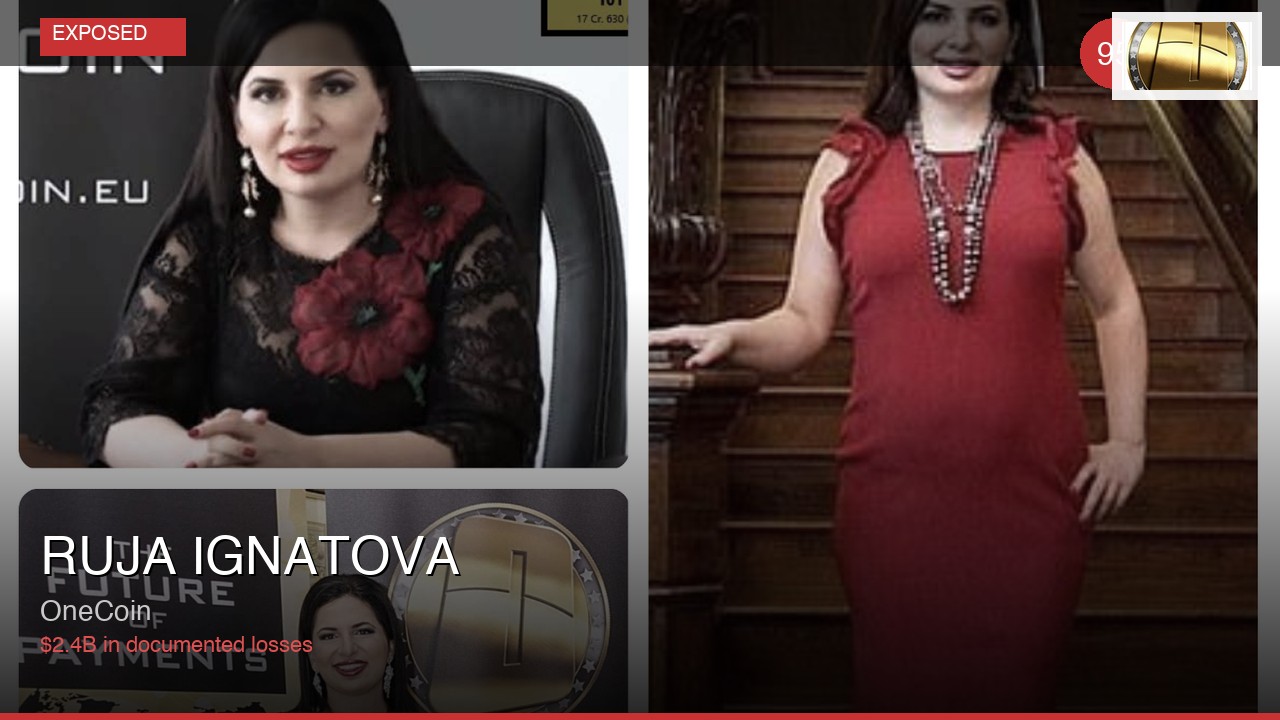

Ruja Ignatova

Ruja Ignatova